Darren415

This text was first launched to Systematic Revenue subscribers and free trials on Oct. 1.

Welcome to a different installment of our BDC Market Weekly Overview, the place we focus on market exercise within the Enterprise Improvement Firm (“BDC”) sector from each the bottom-up – highlighting particular person information and occasions – in addition to the top-down – offering an outline of the broader market.

We additionally attempt to add some historic context in addition to related themes that look to be driving the market or that traders must be aware of. This replace covers the interval by means of the final week of September.

You’ll want to try our different Weeklies – protecting the Closed-Finish Fund (“CEF”) in addition to the preferreds/child bond markets for views throughout the broader revenue house. Additionally, take a look at our primer of the BDC sector, with a concentrate on the way it compares to credit score CEFs.

Market Motion

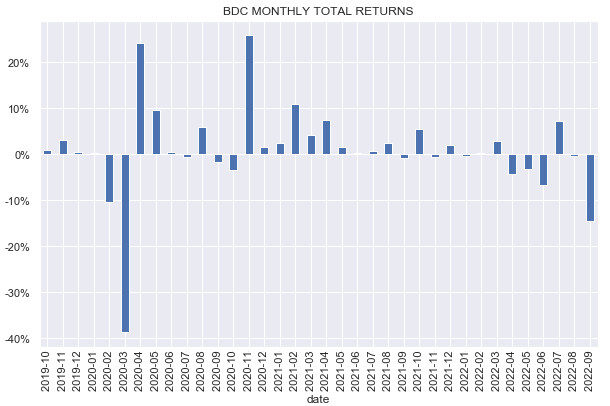

It was a brutal September for BDCs with round a 14% drop. Unusually, BDCs underperformed the broader revenue house in September – solely the mREIT sector posted a worse return.

Systematic Revenue

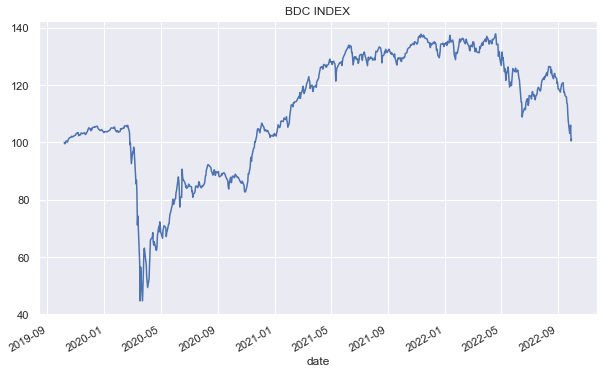

The sector has moved effectively under its June low and is round 28% off its peak. It has additionally executed a roundtrip within the final three years, shifting again to its start line in complete return phrases.

Systematic Revenue

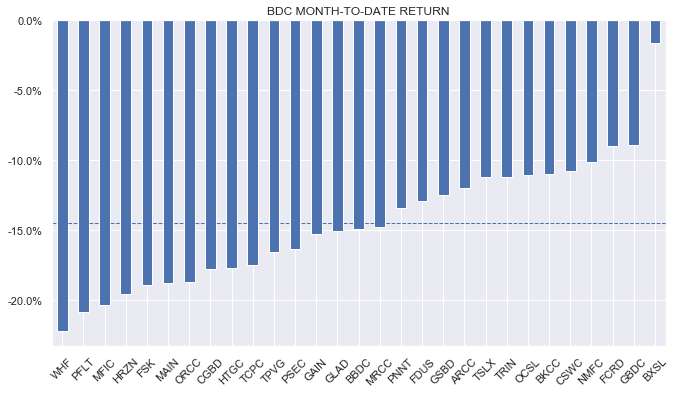

Our holdings comparable to Blackstone Secured Lending Fund (BXSL), Golub Capital (GBDC), Trinity Capital (TRIN) and Oaktree Specialty (OCSL) outperformed the sector in September, although they nonetheless confronted important drops.

Systematic Revenue

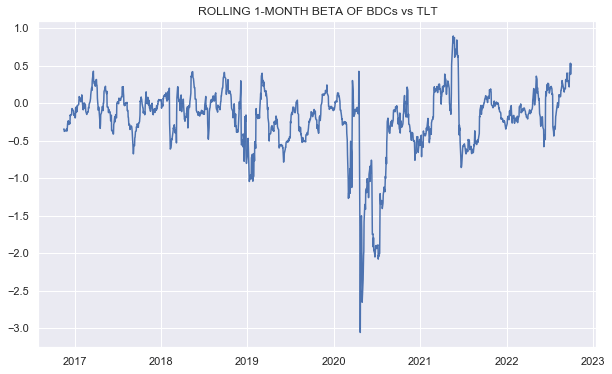

The beta of the sector relative to Treasuries has risen considerably (greater than its beta to shares). There isn’t any apparent cause why this needs to be the case (given the low period profile of BDCs) other than the everyday higher-beta / danger sentiment / recession worries that always trigger BDCs to underperform.

Systematic Revenue

Quick-term charges rose about 0.35% in September – additional elevating the web revenue profile of the sector. Quite a lot of BDCs raised their dividends through the month which suggests sector revenue ranges proceed to rise and that portfolio high quality will not be falling off a cliff.

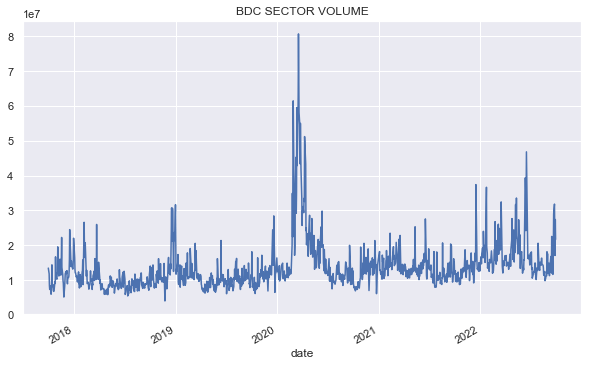

Sector traded quantity rose however stays effectively under its June degree and a fraction of its 2020 degree.

Systematic Revenue

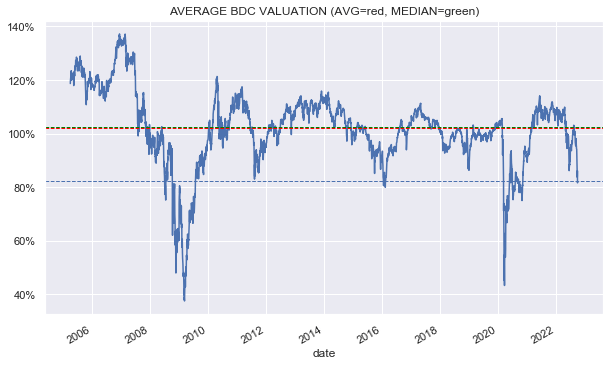

Sector valuation has solely been decrease through the GFC and the COVID crash and is in keeping with the troughs seen through the Euro disaster, the Vitality crash and the Fed auto-pilot tantrum. Given we do not anticipate the subsequent recession to hold existential dangers (not like GFC and COVID), the present sector valuation appears to be like very engaging in mixture. Clearly, this valuation is off a comparatively stale Q2 NAV; nonetheless, default charges stay low and credit score spreads completed Q3 under their Q2 ranges which argues for probably a modest drop in NAVs from Q2.

Systematic Revenue

BDC Software Replace

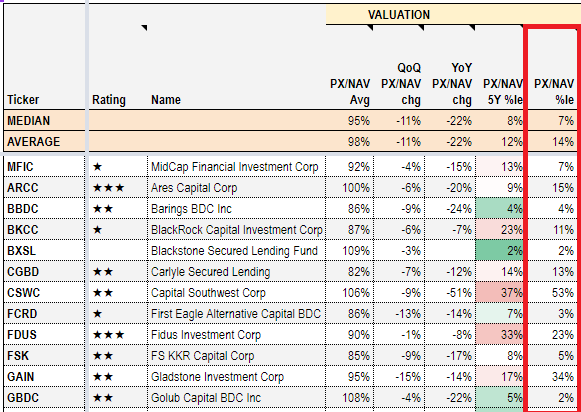

This week we added one other metric to our subscriber BDC Software. The brand new metric captures the given inventory’s historic valuation percentile. Given the sharp drop of the sector in current days, it is notably fascinating to see how the newest valuation compares to its historic degree.

Systematic Revenue CEF Software

The brand new metric known as the PX / NAV %le for brief which stands for the worth / NAV percentile or, merely, the valuation percentile. For example take into account the two% determine for GBDC. What it means is that GBDC has solely traded at a decrease valuation than its present 81% 2% of the time in its historical past. The beginning interval in query is April of 2010 to at present. This implies that GBDC is attractively valued on a relative foundation (i.e. relative to its personal historical past). However, the 53% determine for Capital Southwest (CSWC) exhibits that the present valuation of CSWC is about in keeping with its historic median degree.

Take into account that this metric will not be immediately comparable throughout totally different BDCs as a result of the place to begin for every BDC is totally different (the 5Y percentile determine within the adjoining column is healthier for this objective).

Additionally some BDCs haven’t got a very lengthy public historical past. For instance, whereas the very low determine for TRIN may sign it is particularly low-cost relative to its personal historical past, TRIN solely began buying and selling in 2021 – a interval when BDC valuations have been effectively above present ranges.

Additionally remember the fact that BDCs change. For instance, it’d make sense for a specific BDC to warrant a excessive valuation (if it outperformed the sector earlier in its life) and a decrease valuation (if it has underperformed the sector extra not too long ago).

Stance And Takeaways

This week we took benefit of the air pocket within the sector and added to our BDC allocation by rotating from a fixed-income mutual fund that has held up moderately effectively this 12 months. Particularly, we added to our OCSL place within the Core Revenue Portfolio and to our TRIN place within the Excessive Revenue Portfolio. We additionally see worth in Carlyle Secured (CGBD) and PennantPark Funding (PNNT) at present ranges.